What is The Time Value of Money? (+Easy to Use TVM Tool)

What is the time value of money, and why is it important to you? Read everything about TVM here.

Would you receive $2,000 today, or instead, would you have the guarantee that you would receive it a year from now?

It sounds like a slick question, as you will still receive the $2,000 in both cases.

Still, if you responded like us, we would rather receive it now; you made the right choice. But why would receiving $2000 now be more significant than in a year?

It is all about the notion of the time value of money, or TVM, which plays a massive part in company decision-making.

What is The Time Value of Money?

TVM is an essential financial principle stating that your cash is worth more now than in the future.

So, the value of money relies on how long you wait to spend it; the sooner you employ it, the more beneficial it will be.

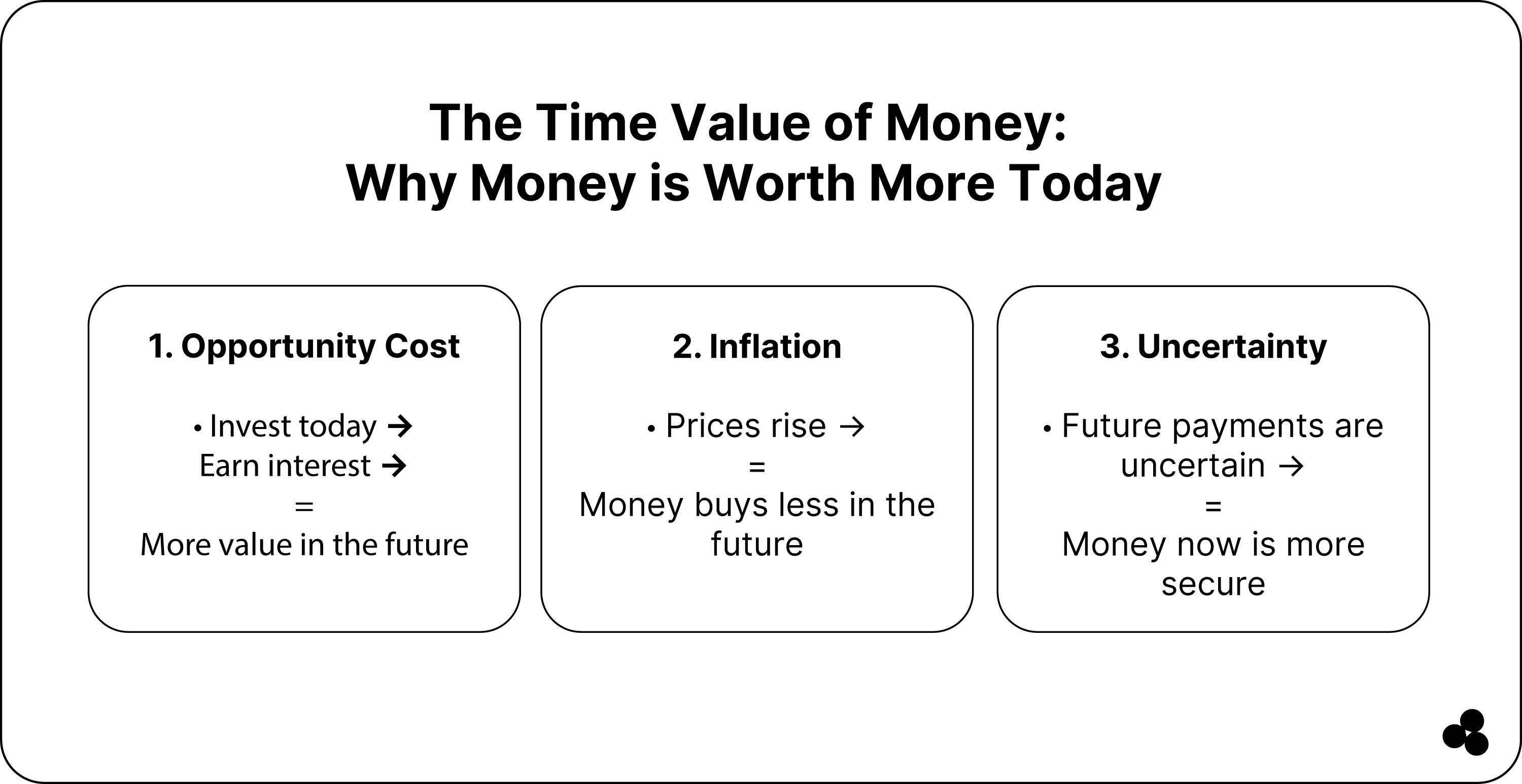

When you look at the financial accounting course presented by Harvard Business School, they present three explanations for why this is so true:

- Provides Opportunity Cost: You can invest your current money and accrued interest to boost its worth.

- Inflation: Still, your money can be less in the near future compared to today.

- Uncertainty: Investing money always involves uncertainty, as something can happen before you receive it.

Still, when time is the sole differentiation facet, the cash you receive momentarily will always have more value. However, certain factors can also play a role at other times.

For example, what is more valuable than having $2000 today or $4000 a year from now? A TVM calculation will translate all your future currency to a present value so you can compare the value and make informed decisions about your finances.

Yet, a worthy note is that your cash flow represented at various periods is only analogous to your cash flow expressed in diverse currencies. So, in financial accounting, you must add (+) or subtract (-) your cash flows from the different currencies.

You first need to convert them to the same currency. Likewise, you can add (+) or subtract (-) cash flows from different periods only if you convert them to your present period.

How to Calculate TVM?

When you use the TVM concept, the dollar you receive today is worth more than receiving it later. For this reason, the time value of money is the most fundamental concept in corporate finance.

Hence, receiving money today is more valuable than receiving the same amount later. This brings us back to the earlier points mentioned in the "What is the time value of money" section.

In the TVM theory, there are two essential reasons: opportunity cost and inflation. For example, you have capital on hand and can invest it into different projects to get a higher return, hence the opportunity cost of the money.

Still, as we all know, there are always risks you must consider, like inflation, that can leave you bankrupt in the future. Why? As money tends to decline in value over time, resulting from inflation, your purchasing power decreases.

Keeping this in mind, the cash flow you receive in the future with increased uncertainty is worth less than the PV (present value) of your cash flow.

If you take the risk of investing one dollar, you should expect reasonable gains of more than your initial contribution as a return.

So, for every risk you take, you must expect a higher return in exchange.

What Makes The Time Value of Money Important?

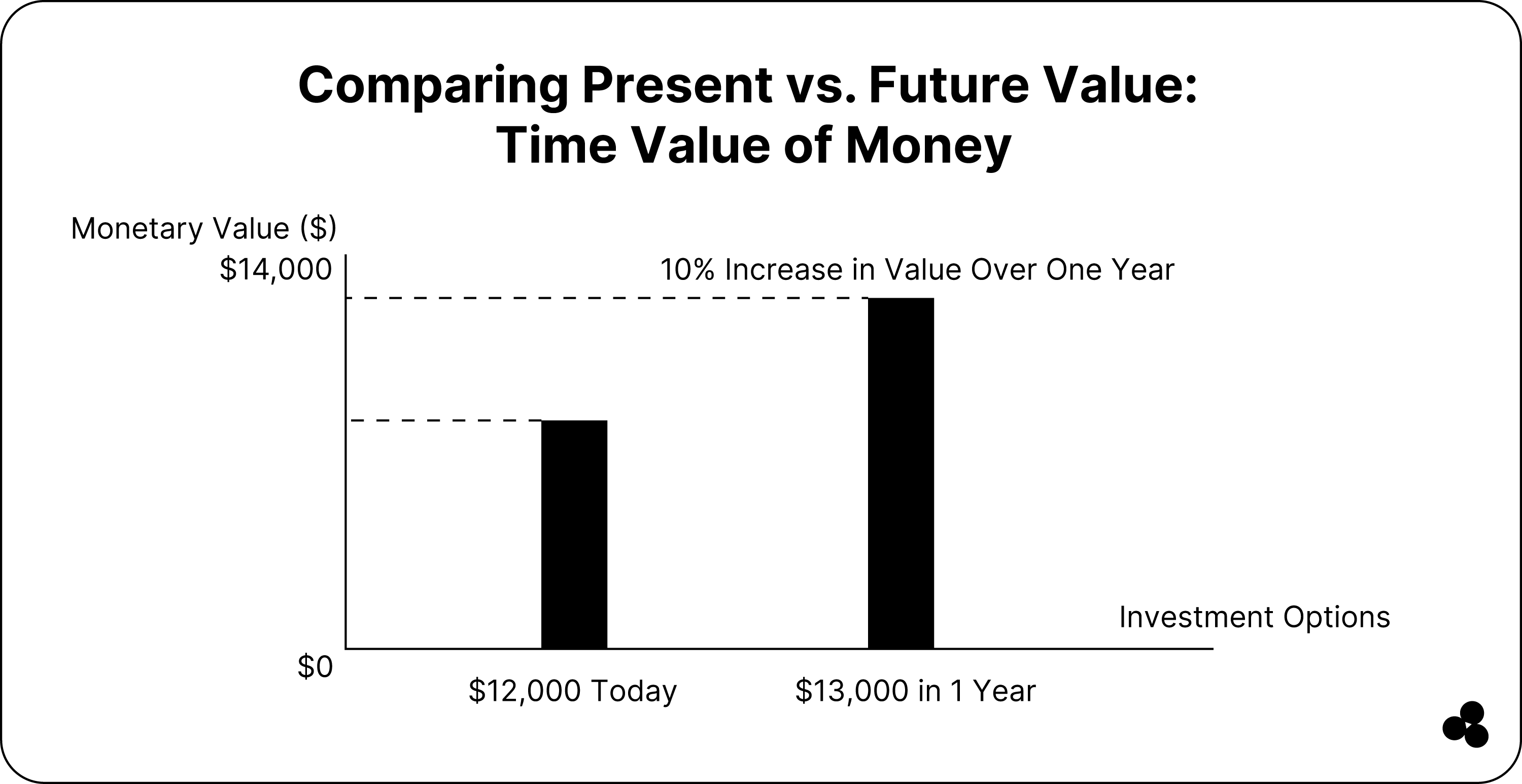

TVM is essential as it is the basis of your NPV (net present value) calculation. Let's use two examples of investment opportunities:

First Option

In your first option, you can receive $12,000 now on this current date.

Second Option

You can receive $13,000, but it will take a year to receive your funds.

So, to make a rational decision, you must evaluate the time value of money to determine your cost of capital (rate of return).

Thus, the $13,000 is 10% more than the $12,000, which serves as the minimum rate of return needed if you are uninterested in the two options.

Still, your returns must exceed those of your first option to make sense of the second option from a financial perspective. For instance, pick the most profitable option if you receive $12,000 on a present date and receive a return greater than 10%.

TVM Formula

When you look at the time value of the money formula of a current date, it is as follows:

The PV is the present value, the FV is the future value, and i is your interest rate (annual rate of return). The n is the number of compounding periods per year, and the t is the number of years.

So, to calculate your future value given your present value, your formula will be:

As with your previous formula, “i” represents the interest rate of your comparable investments.

Examples of Present Value and Future Value Calculations

For instance, if the PV (present value) of your investment is $20 million, and your amount invested is at a 10% rate of return for a year, your FV (future value) will equal to:

FV = $20 million * [1 + (10% / 1] ^ (1 × 1) = $21 million

Still, you can use the same formula to calculate your FV (future value) assuming a quarterly compound interest, for instance, 4.0 times a year:

FV = $20 million * [1 + (10% / 4)] ^ (4 × 1) = $21.04 million

Using a Time Value Money Calculator

While the above is one way to calculate your TVM manually, you can also use Microsoft Excel or Google Sheets. Our Time Value of Money Calculator makes calculations much more straightforward.

Or, if you prefer to use Excel, you can use the subsequent formula:

=PV(rate,nper,pmt,FV,type)

In the formula:

- The “rate” is your discount or interest rate for that period, the same as the “i” in your manual formula.

- NPER is the number of payment terms for your given cash flow and is the same as the “t” in your manual formula.

- FV or PMT is the cash flow or payment to be discounted. Your manual formula uses the FV; you need not enclose values for both.

- The TYPE is when payments are received. If they are accepted at the start of a period, you use 0. If they are received at the end of that period, you use 1.

It is worth noting that this formula considers payments to be equal to your total NPER (number of periods).

Wrap-Up: TVM is Important to Know

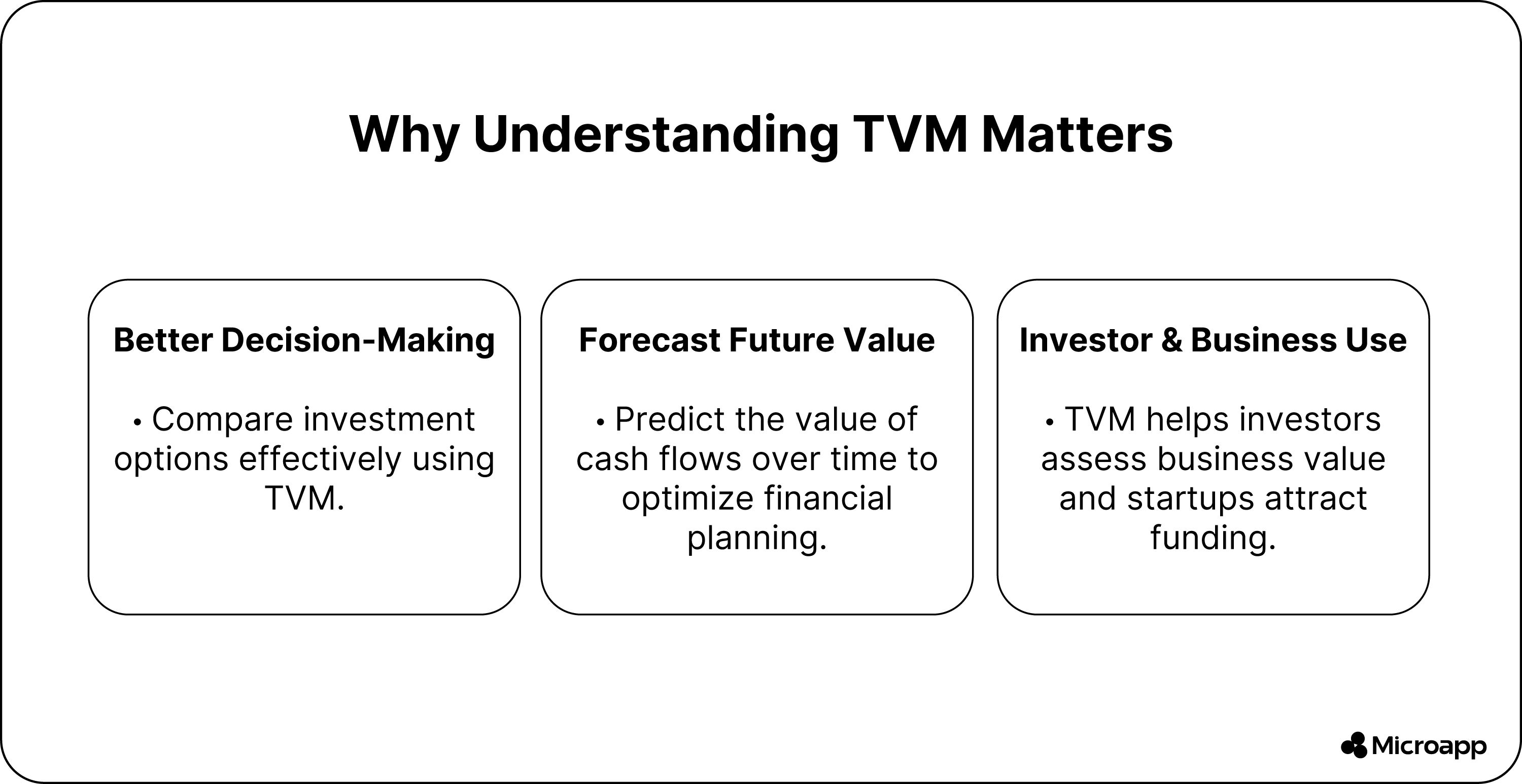

Even if you never need to employ TVM, understanding it can help you decide what projects or endeavors to pursue.

Using the concept of TVM in your forecasts of free cash flows can help you determine the value of your money at a specific time.

You can also use the same formula to predict returns on your present values over multiple projects. Present values you can then compare to decide which provides the most value to your business.

Alternatively, investors use it to assess a business's value established on projected future returns. This helps them determine which investment prospects to prioritize.

The same applies if you are a startup looking for venture capital funding, and it helps to keep this formula in mind.